Financial Strategy

Growth into a Global Specialty Pharma through Strategic Resource Allocation

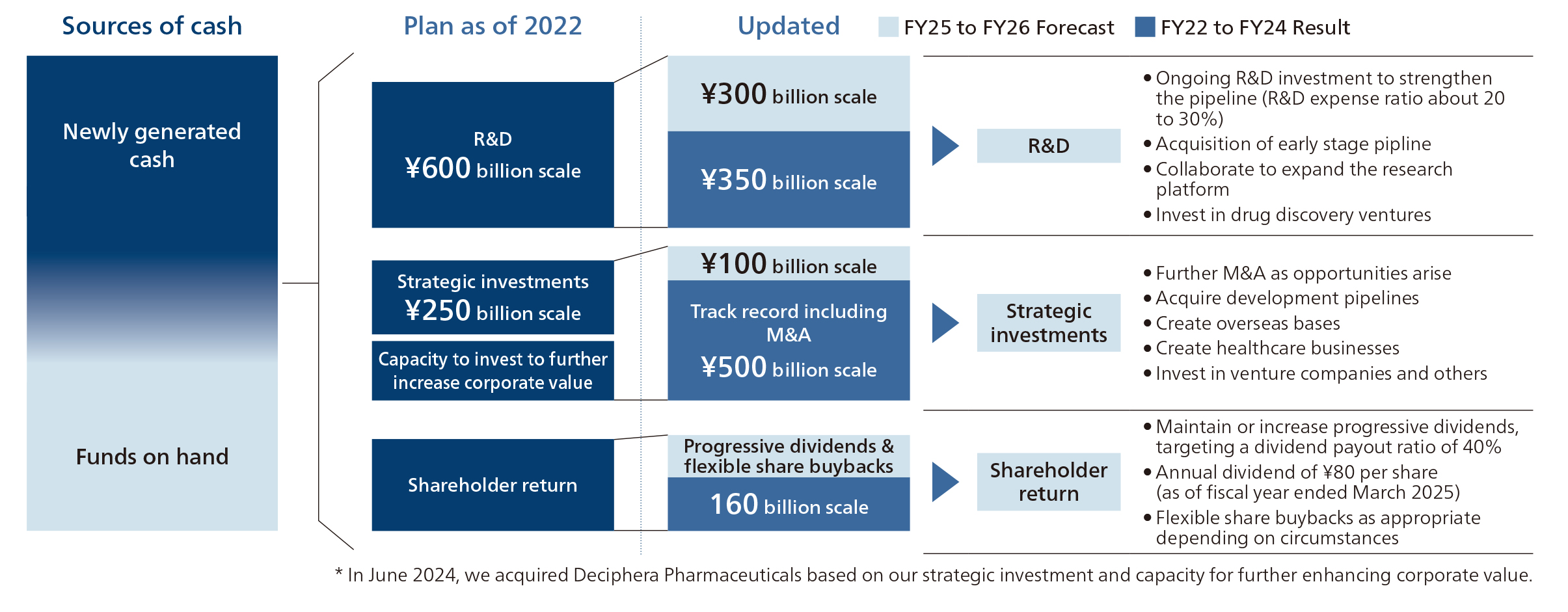

Our company aims to grow into a “Global Specialty Pharma” delivering innovative medicines to patients worldwide. To achieve this, our financial strategy is not merely about reaching numerical goals, but plays the role of “strategic resource allocation” directly linked to the realization of our management vision. Under top management by our executive team, we are building a system that balances financial soundness and growth, by making investment decisions based on capital efficiency indicators such as ROIC (Return on Invested Capital). In FY2024, through the acquisition of Deciphera, which has strengths in oncology in the U.S., we have achieved geographical diversification and expanded our business model as growth drivers. At the time of acquisition, Deciphera had global sales track records for its products and held one new drug candidate under regulatory review in the U.S. and Europe, plus three additional new drug candidates in development. The acquisition of Deciphera greatly contributed to our growth strategies of “Realization of direct sales in the U.S. and Europe” and “Reinforcement of pipelines.” Based on the Deciphera acquisition, we have updated our growth strategy to “Expansion and acceleration of direct sales in the U.S. and Europe,” and by leveraging Deciphera’s capabilities, we aim to achieve further corporate growth. We anticipate Deciphera’s turnaround to profitability in FY2027, continuing efforts to ensure that the success of the acquisition translates directly into enhanced overall corporate value.

Overview and Progress of Financial Strategy in Growth Strategy

Ono’s Financial Policy

●Emphasizing Capital Efficiency and Financial Soundness

Emphasizing Capital Efficiency and Financial Soundness We use capital efficiency indicators such as ROIC and ROE, and pursue profitability that exceeds our capital cost (around 6%). We prioritize mediumto long-term value creation over short-term profits.

●Execution of Strategic Resource Allocation

We invested approximately ¥850 billion (¥350 billion in R&D + ¥500 billion in strategic investments) from FY2022 to FY2024. We plan to invest a total of approximately ¥400 billion in FY2025 to FY2026 as well.

●Shareholder Return and Capital Structure Optimization

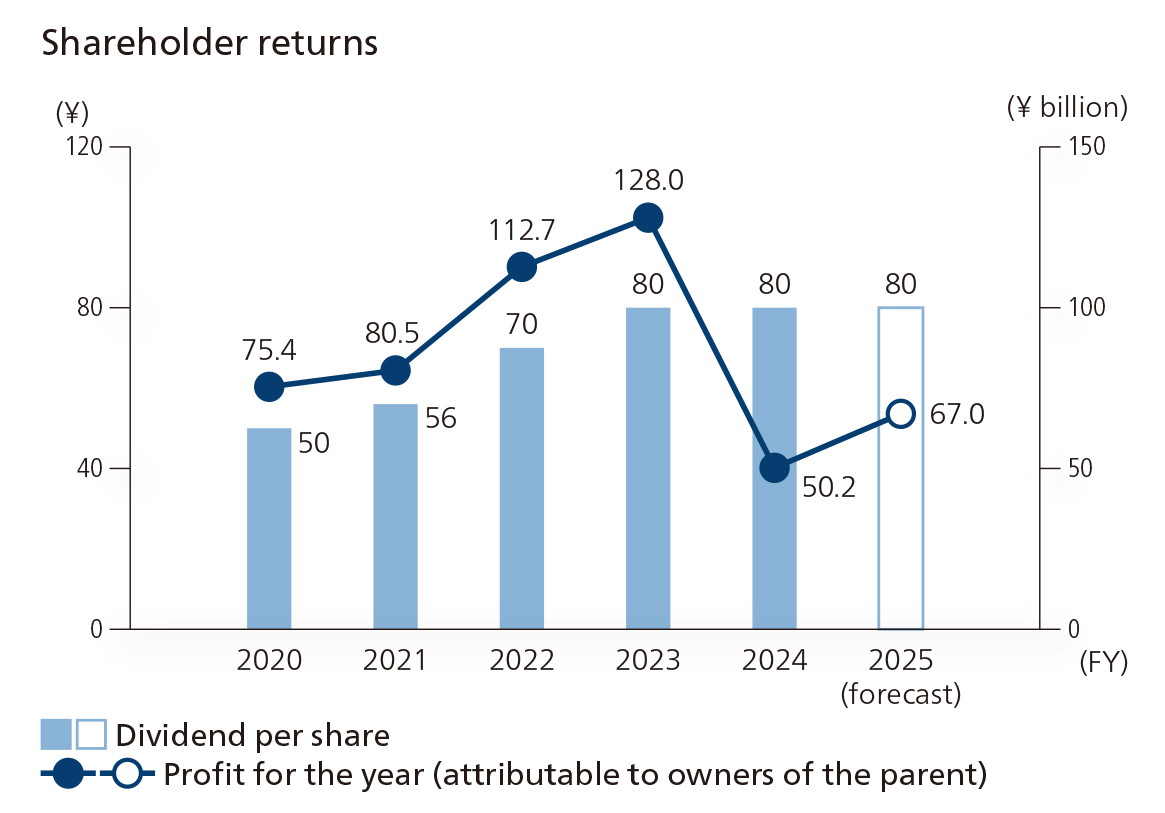

With a progressive dividend policy (2025 forecast: ¥80 per share), we will reduce the ratio of cross-shareholding.

Overview of Growth Strategy

●Accelerate Global Expansion

Through the acquisition of Deciphera, we have expanded our direct sales structure in the U.S. and Europe. Profitable turnaround expected in FY2027, which is anticipated to be a medium- to long-term growth engine.

●Focused Strengthening of R&D

By integrating our own drug discovery and acquired assets in oncology, immunology, and neurology, we aim to improve efficiency and success rates. Several products are in the final stages of development toward FY2025.

●Flexible and Dynamic Strategic Evolution

We regularly review our growth strategies and incorporate external growth such as M&A to ensure flexibility and scalability, advancing toward becoming a Global Specialty Pharma.

Growth strategy targets (FY2022–2026)

|

|

FY2021 result |

FY2022 result |

FY2023 result |

FY2024 result |

FY2025 forecast |

FY2026 target |

|---|---|---|---|---|---|---|

|

Revenue (¥ billion) |

361.4 |

447.2 |

502.7 |

486.9 |

490 |

Revenue CAGR* |

|

Operating profit margin |

28.6 |

31.7 |

31.8 |

12.3 |

17.3 |

Maintain 25% or higher |

|

R&D expenses (¥ billion) |

75.9 |

95.3 |

112.2 |

149.9 |

150 |

ー |

|

R&D expense ratio (% of revenue) |

21 |

21.3 |

22.3 |

30.8 |

30.6 |

20-25% |

*Compared to FY2021

Advancements in Cash Allocation

Over the three years from FY2022 to FY2024, Ono Pharmaceutical invested approximately ¥350 billion in R&D expenses and about ¥500 billion in strategic investments. For the next two years, FY2025 to FY2026, we anticipate investing about ¥300 billion in R&D and approximately ¥100 billion in strategic investments such as M&A and pipeline acquisition. These investments prioritize mediumto long-term value creation over securing short-term profit. Our cash allocation policy is to “pursue growth returns that exceed ROIC” and “balance this with financial soundness.” With respect to acquisitions, although the upfront acquisition costs were substantial, in exchange, we have acquired stable, long-term cash flows as well as difficultto-quantify positive elements such as strengthened sales infrastructure, development infrastructure, and R&D capabilities. These enhancements have also contributed to greater negotiating power in global license deals.

Updated investment allocation (FY2022 to FY2026)

Shareholder Return and Improved Capital Efficiency

At our Company, securing profitability above the cost of capital and improving capital efficiency are positioned as important management indicators, and we are working continuously to improve ROE. Currently, we estimate our cost of capital to be around 6%, and, in FY2024, we managed to secure an ROE just above that level. For FY2025, which is underway, ROE is expected to reach 8%, ensuring profitability that exceeds the “minimum capital cost level” sought by domestic and international investors. However, management is not satisfied with this level, and we are aiming for ROE above 10% in the medium to long term. In particular, if the ongoing M&A of Deciphera is successfully monetized, we expect an even higher level from FY2027 onward. On the other hand, it is not easy to dramatically improve profitability in the short term, and the impact of capital policies such as share buybacks on ROE is limited. Therefore, while aiming for more substantive improvements in profitability, our Company clearly states its “progressive dividend policy,” clarifying our commitment to providing long-term returns to shareholders. This stance has been highly praised particularly among individual investors and helps strengthen trust with investors. By thus advancing our growth strategy and increasing income gains, we aim to sustainably enhance corporate value, boost market evaluations, and increase TSR. Additionally, as part of our efforts to improve capital efficiency, we have been actively reducing cross-shareholdings, and in FY2024, we achieved our goal of reducing the ratio of cross-shareholdings to net assets to less than 10%. We will continue to reduce cross-shareholdings after FY2025 and strive to enhance corporate value by reallocating capital toward growth investments.

We are working on this for the following reasons:

・ Cross-shareholdings are a factor in lowering ROE and ROIC

・ Increasing calls from shareholders to improve capital efficiency

・ Stewardship Code and Corporate Governance Code recommend the sale of shares for which there is no rational reason to hold them.

Going forward, while thoroughly managing with an awareness of the cost of capital, we will continue to strengthen shareholder returns through both dividends and capital policies.

|

Fiscal year |

2020 |

2021 |

2022 |

2023 |

2024 |

2025(forecast) |

|---|---|---|---|---|---|---|

|

Total dividends(¥ billion) |

25 |

27.7 |

34.2 |

37.9 |

37.6 |

37.6 |

|

Payout ratio(%) |

33.1 |

34.5 |

30.3 |

30 |

75.1 |

56.1 |

|

Share buybacks(¥ billion) |

- |

30 |

- |

50 |

- |

Undecided |

|

Total return ratio (%) |

33.1 |

71.6 |

30.3 |

69.1 |

75.1 |

Undecided |

Capital Cost and Capital Profitability

We are working on the following measures about Action to Implement Management that is Conscious of Cost of Capital and Stock Price.

Understanding Capital Cost

We are understanding the "cost of shareholder’s equity" as our capital cost.

Analysis and Assessment

Currently, we are actively pursuing strategic investments to overcome the industry-specific challenge of the expiration of our main product’s patent and to achieve sustainable growth. As we are in the investment phase for future growth, we expect a temporary decline in capital profitability, ROE, which we analyze as one of the factors causing our PBR, a market valuation indicator, to remain around 1x. Meanwhile, our growth strategy is steadily progressing.

Our growth strategy aims to overcome the patent expiration of OPDIVO in 2031 and to become a “Global Specialty Pharma.” We are committed to maximizing the value of existing products and securing resources for growth investments, and our sales are steadily being recorded. The entire group is working together to reinforce our pipeline. Furthermore, we aim to successfully conduct clinical trials in the United States and Europe, obtain regulatory approvals, achieve direct sales in these large markets, and accelerate our global expansion.

In June 2024, we acquired Deciphera Pharmaceuticals, thereby adding two products to our portfolio: QINLOCK, a treatment for gastrointestinal stromal tumors approved in over 40 countries including the US and Europe, and ROMVIMZA, a novel treatment for tenosynovial giant cell tumor launched in the US in February 2025. In July 2025, we will integrate our development and sales bases in the US and Europe into Deciphera, and going forward, we will accelerate our global expansion centered on Deciphera.

Tirabrutinib, which is being developed for primary central nervous system lymphoma with the aim of launching in the US, has progressed to a stage where market launch is expected, and is anticipated to contribute to our global expansion. Furthermore, sapablursen, a promising compound for the treatment of the rare disease polycythemia vera, is expected to have a high probability of success due to its mechanism of action, and is highly anticipated to accelerate our global expansion. If we are able to launch multiple products globally from our pipeline currently under evaluation in approximately 10 ongoing PoC (Proof of Concept) trials—early-stage clinical trials to confirm whether the safety and efficacy anticipated in the drug discovery stage are realized in clinical settings—or from pipelines acquired through ongoing licensing activities and acquisitions, we will be able to overcome the OPDIVO patent expiration and ensure further growth.

In addition, to further reduce the implied cost of shareholders’ equity over the medium to long term, we will continue not only to deliver results from growth investments, but also to advance ESG initiatives, strengthen governance to mitigate management risks, invest in human capital, and enhance employee engagement.

We will continue to steadily advance toward our long-term vision of becoming a “Global Specialty Pharma.”

Continued Efforts

We will continue to promote management that is conscious of capital costs and stock price, and strive for proactive disclosure and dialogue with investors. For specific efforts and other details, please refer to our corporate report.

Corporate Report (Financial Strategy and Resource Allocation)

Refer to pages 29–32 for more information.

Indicators (Actual Results)

*After Tax %

|

Indicators |

2020 |

2021 |

2022 |

2023 |

2024 |

|

|---|---|---|---|---|---|---|

|

Capital Cost |

Cost of Shareholder’s Equity * |

Approximately 6% (Based on CAPM) |

||||

|

Capital Profitability |

ROE |

12.6% |

12.5% |

16.1% |

16.7% |

6.4% |

|

Market Evaluation |

PBR |

2.27x |

2.28x |

1.82x |

1.45x |

0.96x |